Federal Treasurer Scott Morrison put forward a number of proposed changes, mainly around contributions to superannuation and taxation, in the budget last night.

Here’s a brief roundup of what the proposals could mean for you—whether you’re starting out in your career, taking care of a family, on the cusp of retirement or enjoying life after work.

Remember, proposals are not set in stone and could change as legislation passes through parliament.

Superannuation

Reduced cap on before-tax super contributions

The government has proposed that from 1 July 2017 the concessional (before-tax) contributions cap be cut from $30,000 (or $35,000 for people over the age of 49) to $25,000 per year for everyone, irrespective of age.

Ability to catch up on before-tax super contributions

The government has proposed that from 1 July 2017 that individuals with a super balance of less than $500,000 be allowed to make additional before-tax contributions where they have not reached their concessional contributions cap in previous years.

Lifetime cap on after-tax super contributions

The government has proposed that from 3 May 2016 the cap on non-concessional (after-tax) super contributions—which is currently $180,000 per person, per financial year—be replaced with a $500,000 lifetime cap.

The lifetime cap, if introduced, would take into account all non-concessional contributions made on or after 1 July 2007, with excess contributions being subject to tax or removed from the super system.

Those who have exceeded the $500,000 limit prior to budget night will not be penalised or required to remove any contributions, however, future non-concessional contributions will be classed as excessive.

Reduced threshold for high-income earners

The government has proposed that from 1 July 2017, the high-income concessional contributions tax rate of 30%, which is double the 15% paid by most workers, will apply to those earning an annual income above $250,000. Currently the annual income threshold is $300,000.

Removal of the work test for voluntary super contributions

The government has proposed that from 1 July 2017 individuals under the age of 75 will no longer need to meet the work test. Under current requirements, those aged between 65 and 74 must have worked for a set period of time in the financial year to be able to make voluntary super contributions.

Introduction of the Low Income Super Tax Offset

Since July 2012, individuals with an income of up to $37,000 automatically received a government contribution of up to $500 paid directly into their super. This arrangement expires on 30 June 2017.

In order to replace this, the government has proposed that from 1 July 2017, it will introduce a Low Income Super Tax Offset. This will allow individuals with a total income of up to $37,000 to receive a tax refund up to $500 of the tax paid on their concessional contributions.

Making spouse contributions more attractive

Currently, an individual making a contribution into their spouse’s super account is entitled to a maximum tax offset of $540 if certain requirements are met.

The government proposes to increase access to the spouse super tax offset by raising the lower income threshold for the receiving spouse from $10,800 to $37,000.

Changes to transition to retirement strategies

Investment earnings on super fund assets that support a pension are currently tax free, however the government has proposed that from 1 July 2017 this will no longer apply to transition to retirement income streams.

This means that earnings on fund assets supporting a transition to retirement strategy after this date will be subject to the same maximum 15% tax rate applicable to an accumulation fund.

For tax purposes you can also currently elect for certain super income stream payments to be taxed as lump sums, but the government is proposing to also remove this option.

Introduction of a $1.6 million super transfer balance cap

The government is proposing to introduce a $1.6 million transfer balance cap from 1 July 2017.

This cap will limit the total amount of accumulated super benefits that an individual can transfer into the retirement income phase. Subsequent earnings will not form part of this cap.

Where an individual transfers super amounts in excess of $1.6 million, or are already in the retirement income phase with a balance above $1.6 million, they’ll be able to maintain the excess amount in a super accumulation account where earnings will be taxed at the concessional rate of 15%.

Taxation

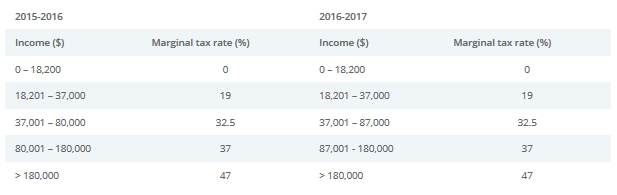

Changes to marginal tax rates

A tax cut has been proposed at the current $80,000 taxable income threshold.

As a result, marginal tax rates for resident taxpayers are proposed to change as follows:

Want to know more?

Please contact us on ph 07 4659 9881.

Or go to www.budget.gov.au.

And remember, the proposals may change as legislation passes through parliament.

Source: AMP 4th May 2016